Last week the DOJ filed a lawsuit to block Visa’s proposed $5.3B acquisition of Plaid which was announced in January. The complaint had to be creative because Visa & Plaid don’t really compete today but the DOJ held no punches. Throughout the complaint they harp on Visa’s monopolistic position as it pertains to online payments, the significant barriers to entry competitors would have entering the market, and the two sided network effect they’ve developed between both consumers & merchants.

Visa seeks to buy Plaid — as its CEO said — as an “insurance policy” to neutralize a “threat to our important US debit business.” Visa is a monopolist in online debit transactions, extracting billions of dollars in fees annually from merchants and consumers. Plaid, a financial technology firm with access to important financial data from over 11,000 U.S. banks, is a threat to this monopoly: it has been developing an innovative new solution that would be a substitute for Visa’s online debit services. By acquiring Plaid, Visa would eliminate a nascent competitive threat that would likely result in substantial savings and more innovative online debit services for merchants and consumers.

Visa is “everywhere you want to be.” Its debit cards are accepted by the vast majority of U.S. merchants, and it controls approximately 70% of the online debit transactions market.

American consumers use debit cards to purchase hundreds of billions of dollars of goods and services on the internet each year. Many consumers buying goods and services online either prefer using debit or cannot access other means of payment, such as credit. Because of its ubiquity among consumers, merchants have no choice but to accept Visa debit despite perennial complaints about the high cost of Visa’s debit service

Visa’s monopoly power in online debit is protected by significant barriers to entry and expansion. Visa connects millions of merchants to hundreds of millions of consumers in the United States. New challengers to Visa’s monopoly would thus face a chicken-and-egg quandary, needing connections with millions of consumers to attract thousands of merchants and needing thousands of merchants to attract millions of consumers. Visa’s Chief Financial Officer has acknowledged that building an extensive network like Visa’s is “very, very hard to do” and “takes many years of investment,” but “[i]f you can do that, then you can have a business [like Visa’s] that has a relatively high margin.” He explained that entry barriers are so significant that even well-funded companies with strong brand names struggle to enter online debit.

Mastercard, Visa’s only longstanding rival in online debit services, has a much smaller market share of around 25%. For years, Mastercard has neither gained significant share from Visa nor restrained Visa’s monopoly. Mastercard’s participation in the online debit market has not translated into lower prices for consumers, and this appears unlikely to change. For example, Visa has long-term contracts with many of the nation’s largest banks that restrict these banks’ ability to issue Mastercard debit cards. Visa also has hamstrung smaller rivals by either erecting technical barriers, or entering into restrictive agreements that prevent rivals from growing their share in online debit, or both.

These entry barriers, coupled with Visa’s long-term, restrictive contracts with banks, are nearly insurmountable, meaning Visa rarely faces any significant threats to its online debit monopoly. Plaid is such a threat.

While Plaid’s existing technology does not compete directly with Visa today, Plaid is planning to leverage that technology, combined with its existing relationships with banks and consumers, to facilitate transactions between consumers and merchants in competition with Visa. Like Visa’s online debit services, Plaid’s new debit service would enable consumers to pay for goods and services online with money debited from their bank accounts

Visa feared that Plaid’s innovative potential — on its own or in partnership with another company — would threaten Visa’s debit business. In evaluating whether to consider Plaid as a potential acquisition target in March 2019, Visa’s Vice President of Corporate Development and Head of Strategic Opportunities expressed concerns to his colleagues about the threat Plaid posed to Visa’s established debit business, observing: “I don’t want to be IBM to their Microsoft.” This executive analogized Plaid to an island “volcano” whose current capabilities are just “the tip showing above the water” and warned that “[w]hat lies beneath, though, is a massive opportunity — one that threatens Visa.” He underscored his point by illustrating Plaid’s disruptive potential:

While conducting extensive due diligence, Visa’s senior executives became alarmed to learn about Plaid’s plans to add a “meaningful money movement business by the end of 2021” that would compete with Visa’s online debit services

Visa’s senior leadership estimated a “potential downside risk of $300–500M in our US debit business” by 2024 should Plaid fall into the hands of a rival. Visa understood that could create an “[e]xistential risk to our U.S. debit business” and that “Visa may be forced to accept lower margins or not have a competitive offering.”

Visa offered approximately $5.3 billion for Plaid, “an unprecedented revenue multiple of over 50X” and the second-largest acquisition in Visa’s history. Recognizing that the deal “does not hunt on financial grounds,” Visa’s CEO justified the extraordinary purchase price for Plaid as a “strategic, not financial” move because “[o]ur US debit business i[s] critical and we must always do what it takes to protect this business.”

While never the intended use case, due to access to internal documents that the public otherwise would never be privy to, antitrust complaints from the FTC or DOJ often serve as terrific “investment advice.” If a merger is blocked due to antitrust concerns, it’s always insightful to analyze any disclosed information around market share estimates / data, pricing power, etc… and determine what type of moat / network effect the acquirer and or acquirer coupled with the target have together.

The DOJ highlights that online sales grew 30% between 1Q & 2Q20 as a result of COVID-19 and that American consumers use debit cards to purchase hundreds of billions of dollars of goods & services each year. So you have an 11 figure + market that’s growing at a double digit rate and one company has 70%+ market share? On the surface that seems like a great investment opportunity. Anyone familiar with V’s business knows about the network effects V enjoys with EBITDA / NI margins expanding from 27.1% / 13.5% in 2005 to 70.3% / 54.0% in ‘20E.

This got us to look at financial service companies more broadly beyond the card networks & what constitutes a moat / network effect.

Moats & Network Effects

There has been a lot written about moats & network effects in across all types of businesses & industries. Warren Buffett used the term to convey the idea of a company’s competitive advantage:

“In most businesses you see high returns on capital decrease over time as competition comes in. However, there is a very small minority of businesses that enjoy many years of high returns on capital. They essentially beat the odds. They defy economic gravity. And the question simply becomes, how? And in my view, it’s because they’ve created structural advantages, economic moats — a way of insulating themselves, buffering themselves against the competition — which enables them to maintain supernormal returns on capital longer than academic theory.”

Pat Dorsey the former director of Equity Research at Morningstar, Head of Dorsey Asset Management, and author of The Five Rules for Successful Stock Investing and The Little Book that Builds Wealth has written at length about moat businesses. Pat states that companies generally build sustainable competitive advantage through either product differentiation, real or perceived, driving costs down, locking in customers with high switching costs, or locking out competitors through high barriers to entry. Pat has a great interview with The Manual of Ideas where he talks about moats.

He describes four major ways a company can establish an economic moat: (i) Intangible Assets (ii) High Switching Costs (iii) Network Effect, and (iv) Cost Advantages.

· Intangible Assets- firms can create moats by preventing other companies from duplicating a good or service. This can be achieved by having intangible assets that do not have a physical form but do produce value. The examples of these assets are brands, patents and licenses that are hard for competitors to match.

o Dorsey feels one of the most common mistakes investors make is that they assume well-known brands offer competitive advantage. A brand can be considered a moat only if it increases the consumer’s willingness to pay, lowers search costs and attracts them to buy its product again.

· High Switching Costs- there are businesses that have a valuable competitive advantage of having high switching costs and they outweigh the cost or product benefits of a new and better product. Customers find it difficult to switch to a competitor easily, giving these firms a pricing power. Most common examples of these businesses are banks and famous software vendors as customers do not want to go through the hassles of transferring an account or training an entire staff on a new piece of software.

· Network Effect- the network effect is another form of moat that creates value for businesses. These types of companies have an already-running distribution network for their product and tend to create natural monopolies and oligopolies, because it is challenging in terms of cost and effort for other companies to get a distribution network set up.

o These businesses work on the principle that the value of a particular good or service increases for both new and existing users as more people use that good or service.

o Dorsey believes the network effect works well due to non-linearity of nodes v/s connection and radial network is less valuable than interactive network.

§ “If you have a web, and the number of nodes in that web goes from one to two to three to four, the number of connections increases exponentially. So that is something that makes it very hard to replicate a network once the network gains scale. One thing you want to watch out for, though, is a radial versus interactive networks. A radial network is less valuable as a series of channels, a series of spokes of different nodes are easier for a competitor to pick off by underpricing service in that node. So radial networks are much, much less robust than interactive ones.”

· Cost Advantages- if a business can figure out ways to provide a good or service at a relatively low cost then it can create a cost advantage from its competitors, especially in an industry where price is the most important factor.

o These businesses can be termed as moats as they can undercut their rivals on price. There are a number of ways companies can accomplish this like having a better business model than the competitors, having a unique asset over competition, having better locations, better access to resources, and better processes. All these factors help a company to cut costs in ways that their competitors cannot

Dorsey also notes that moats can & do erode over time. Technological change is one of the biggest factors why there can be erosion in a moat. When a new technology arrives, there is usually an opportunity for a competitor to erode the moat of another company. Poor management decisions can also lead to erosion of moat.

Brian Feroldi over at the Motley Fool also has some good thoughts on this as part of his investment framework to decipher whether or not a company is “high-quality” with Moats being part of his criteria including:

· Wide vs. No Moat- Brian includes sources of a moat such as: (i) Network Effect (ii) Switching Costs (iii) Low-Cost (iv) intangible and (v) Counter-positioning into his framework.

· Widening or Narrowing Moat- Brian assesses the pace of either the widening or narrowing of a moat.

The idea of attempting to quantify the pace of change of a moat is important particularly given the pace of technological disruption across so many industries.

Central Nervous System (“CNS”) vs. Appendix Stocks- Enterprise SaaS

In June we published a piece entitled This Time It’s Different: Maybe? where we looked at what was going on with Cloud / SaaS stocks in the midst of the pandemic. We noted that Bob Smith famously said, “Software contracts are better than first-lien debt. You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.” We also highlighted Michael Milken who when discussing Smith / Vista Equity & B2B software called it the “Central Nervous System” equivalent for many companies.

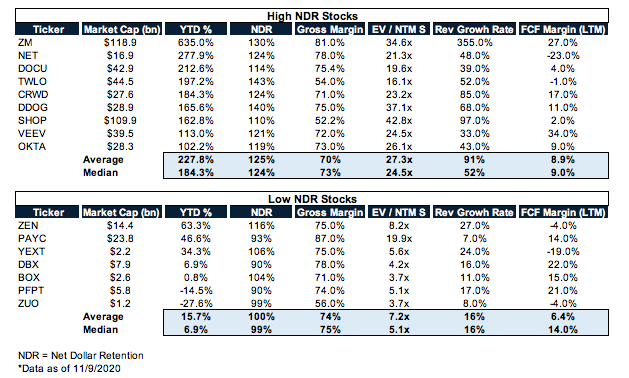

We looked to quantify “CNS” stocks by analyzing Net Dollar Retention & Churn for these SaaS companies. A screen based solely on NDR showed the market was doing a good job bifurcating those companies that were “mission critical” software vs. software that was nice to have which usually had some combination of high switching costs and / or network effects. The “High NDR” stocks had an average / median return YTD of 227.8% / 184.3% vs. the “Low NDR” stocks at 15.7% / 6.9% respectively.

Financial Services Moats

After Visa’s acquisition was initially announced we wrote a piece entitled The Plaid for X: What’s Next For FinTech Infrastructure, where we discussed a number of legacy infrastructure providers in financial services that have enjoyed moats in their core business offerings for the better part of 50+ years spanning the spectrum of (i) Intangible Assets (ii) High Switching Costs (iii) Network Effects & (iv) Cost Advantages.

In the below comp table we look at 20 companies across Asset Management, Banking / Payments, Custody, Clearing / Settlement, Data, Exchanges, and Mortgages that account for $1.3T in market cap, $150B+ in revenue, $38.0B+ in net come with an average age of 51.5 years old. As you dig through 10K’s, earnings calls & investor presentation transcripts you often see / hear words such as “Brand,” “Distribution,” “Scale,” “Cost Advantage,” “Network Effect,” etc…

Asset Management

· Broadridge (BR)- Broadridge processes on average over $7.0 trillion in equity and fixed income trades per day in the US / Canada. They processed ~80% outstanding shares in the US for proxy services, they provide trade processing to 19 of the 24 primary dealers of Fixed income, and process over 6 billion investor & customer communications.

o BR has a moat due to network effects.

· SS&C (SSNC)- SS&C is the world’s largest hedge fund & PE administrator as well as the largest mutual fund transfer agent. SS&C’s business model combines end-to-end expertise across financial services operations with software and solutions to service even the most demanding customers in the financial services and healthcare industries. SS&C owns and operates the full technology stack across securities accounting, front-to-back-office operations, performance and risk analytics, regulatory reporting, and healthcare information processes.

o SSNC has a moat due to intangible assets (brand) + cost advantages.

Banking / Payments

· FIS (FIS) / Fiserv (FISV) / Jack Henry (JKHY)- FIS / FISV / JKHY are the “Big 3” providers of core bank technology and do business with 90% of US banks with <$1.0B in Assets.

o FIS describes itself as a “leading provider of technology solutions for merchants, banks, and capital markets firms globally. Our over 55,000 employees are dedicated to advancing the way the world pays, banks and invests by applying our scale, deep domain expertise and data-driven insights.”

o FISV describes itself as “a leading global provider of financial services technology. We serve clients around the globe, including banks, credit unions, other financial institutions and merchants. We provide account processing systems; electronic payments processing products and services, such as electronic bill payment and presentment services, account-to-account transfers, person-to-person payments, debit network solutions, debit card processing and services, general purpose credit, retail private label and commercial credit card processing and services, and payments infrastructure services; internet and mobile banking systems; and related services, including card and print personalization services, item processing and source capture services, loan origination and servicing products, stored value network solutions and fraud and risk management products and services.”

o JKHY describes itself as a “ provider of core information processing solutions for banks. Today, the Company’s extensive array of products and services includes processing transactions, automating business processes, and managing information for nearly 8,700 financial institutions and diverse corporate entities.”

§ These business enjoy a moat due to a combination of (i) High Switching Costs and (ii) Network Effects.

· Global Payments (GPN)- GPN is a “leading pure play payments technology company providing payments and software solutions to approximately 3.5 million merchant locations and more than 1,300 financial institutions across more than 100 countries throughout North America, Europe, Asia-Pacific and Latin America.”

o GPN has a moat due to intangible assets (brand) + cost advantages.

· Mastercard (MA) / Visa (V)- MA & V are the quintessential network effect businesses as illustrated by the DOJ’s complaint. They tend to get more powerful the more users they have; as its accepted at more places, more users signup, the bigger the moat they built up.

Custodians

· Bank of New York Mellon (BK) / State Street (STT)- BK & STT are both 225+ years old and combined have $65.0T+ of AUC/A.

o BK & STT have a moat due to intangible assets / cost advantages.

Clearing / Settlement

· The Depository Trust Company- The DTC provides clearing & settlement to financial markets and claims some ~80% market share of OTC derivatives and has some ~98% of shares held via Cede & Co.

o DTC has a moat due to intangible assets (in this case regulatory moat) which provides a network effect.

Data

· Bloomberg / Factset (FDS) / Thomson Reuters (TRI)- Bloomberg, FDS, and TRI are some of the largest data vendors for Wall Street.

o Bloomberg / FDS / TRI have a moat due to network effects.

Exchanges

· Chicago Board Option Exchange (CBOE) / CME Group (CME) / Intercontinental Exchange (ICE) / Nasdaq (NDAQ)- The exchanges have a moat due to network effects.

Mortgages

· BlackKnight (BKI)- BKI is a leading provider of integrated software, data and analytics solutions to the mortgage and consumer loan, real estate and capital markets verticals. Their solutions facilitate and automate many of the mission-critical business processes across the homeownership lifecycle. Based on publicly available data they claim 59% market share amongst first lien mortgage loans in the U.S., 20% market share for second lien loans, and 51% market share overall.

o BKI has a moat due to high switching costs & network effects.

If we look at the some of the high level financial data / performance data based on the assessed “reason for a moat” you can see those that benefit from Network Effects & Higher Switching Costs enjoy greater EBITDA / NI margins which have driven outperformance over the trailing 3 & 5 years versus those that have a moat as a result of “Intangible Assets” or “Cost Advantages” which have inferior margins & performance data.

While we don’t have banks listed on the above comp table and although there are some 5,066 commercial banks & saving institutions and another 5,091 credit unions there are even moats / network effects in banking with the Top 15 Banks in the U.S. controlling in excess of 50% of total deposits. This is a combination of network effects & intangible assets.

What does this mean for FinTech companies?

There’s an opportunity for FinTech companies to create a better “mousetrap” to serve the financial service industry, clients, and ultimately end users; with a more modern & flexible technology stack. As founders go about building their businesses across the various FinTech sub-sectors think about how, if you can execute on your vision, your company can build a moat due to Network Effects first & foremost followed by the potential for Higher Switching Costs (which is earned not charged), Intangible Assets, and Cost Advantages (e.g., cross-selling products, marketplace vs. single lending source, etc…)